HMRC have heralded a major change to the NHS VAT rules by announcing their intention for the first time to apply ‘penalties for VAT infringements’ for periods beginning on or after 1 April 2011.

There have always been penalties for VAT errors made by other taxpayers but these have never before been implemented in the NHS. The recent introduction of a new penalty regime for all taxpayers has however caused HMRC to conclude that the NHS should be treated no differently.

What are the penalties?

There are a range of VAT penalties for different types of infringement, however the main penalties are for incorrect VAT returns, which can apply where a VAT return contains either a ‘careless’ or ‘deliberate’ inaccuracy (action) which leads to an understatement or over-claim of VAT.

These penalties are designed so that if a taxpayer takes ‘reasonable care’ when completing a return, they will not be penalised for an error, however the definition of reasonable care can vary depending upon the person, their circumstances and their abilities. These can be reduced or eliminated depending upon whether the error is voluntarily disclosed before HMRC discovers it (unprompted) or after HMRC makes enquiries (prompted).

Penalties are expressed as a percentage of the potential lost revenue and can be summarised as follows:

| Reason for penalty | Penalty | Possible reduced penalty for unprompted disclosure | Possible reduced penalty for prompted disclosure |

| Careless action – failure to take reasonable care | 30% | 0% | 15% |

| Deliberate but not concealed action | 70% | 20% | 35% |

| Deliberate and concealed action | 100% | 30% | 50% |

| Error in HMRC assessment | 30% | 0% | 15% |

There are other penalties which may apply for other infringements including such things as issuing incorrect certificates, however HMRC have yet to provide any detailed guidance on how and which of the penalties will be levied to the NHS.

What this Means to the NHS

With the introduction of penalties, it will be more important than ever to have robust and documented VAT procedures in place for the correct accounting of VAT and preparation of VAT returns.

The penalty regime will certainly apply to input tax and output tax errors, so it will be important to ensure that the correct VAT liability is recorded for all business transactions.

Although little detail has been provided to-date, we have also been told that HMRC see no reason why the penalty regime wouldn’t apply to contracted-out services (“COS”) VAT errors, i.e. VAT claimed incorrectly under the COS rules.

There are still quite a few questions unanswered such as whether COS VAT corrections will require ‘disclosure’ to HMRC, or whether the annual June deadline for COS VAT will be extended to four years to allow a ‘level playing field’ for the correction of COS VAT underclaims and overclaims.

We will therefore provide further updates once this information is known.

The ECJ has recently given its judgement on questions from the UK VAT Tribunal in the case of Astra Zeneca, which provided employees with retail vouchers as part of their remuneration.

Astra Zeneca argued that input tax on the purchase of these vouchers should be recoverable as a business overhead but that no VAT was due on the supply of the vouchers as there was no consideration for the supply.

The ECJ found that provision of the vouchers is an economic activity and is a supply of services. They also concluded that the consideration for this supply is the part of the cash remuneration given up by the employee in return for the voucher and that output tax is due on that consideration.

This judgement is likely to lead to a change to the current VAT treatment of benefits provided by employers to employees under salary sacrifice arrangements, whereby output tax will become due on the supply of various types of salary sacrifice benefits which would otherwise be taxable supplies for VAT purposes. The decision could affect types of benefit provided under such schemes as:

- Workplace car-parking

- Cycle schemes

- Lease cars

- Mobile phones

The supply of benefits which would normally be exempt from VAT, such as childcare vouchers, should remain unaffected by the ECJ’s judgement. ‘Bus’ schemes will not be affected because they are zero rated for VAT purposes. Workplace nurseries are also unlikely to be affected since activities undertaken within them are typically exempt for VAT purposes.

Potential Effect on the NHS

Where salary sacrifice schemes such as cycle to work schemes or car-parking have been entered into by NHS bodies, VAT may now become due. However, if any NHS Trusts have historically disallowed input tax on associated purchases of salary sacrifice benefits, this VAT would subsequently become recoverable as business input tax.

This change in VAT treatment may not therefore have any material effect in circumstances where benefits have been charged on ‘at cost’ including the VAT cost, as the revised treatment of declaring output tax and recovering input tax would effectively be cost neutral. This change may however have an adverse effect on benefits where there is little if any input tax to recover, such as staff car-parking.

We will provide more detailed guidance when HMRC confirm how the Astra Zeneca decision should be applied. In the meantime, NHS bodies should review their existing salary sacrifice schemes and flexible benefit schemes to see if the benefits provided are subject to VAT. They should also:

- ensure that any proposed schemes are planned to take account of the potential additional VAT costs

- consider if they will bear the full burden of the additional VAT cost or ask employees to bear all or some of the cost

- note that any increased salary deductions may require changes to employment contracts and will have tax consequences

- consider changing the range of benefits available to mitigate the VAT cost

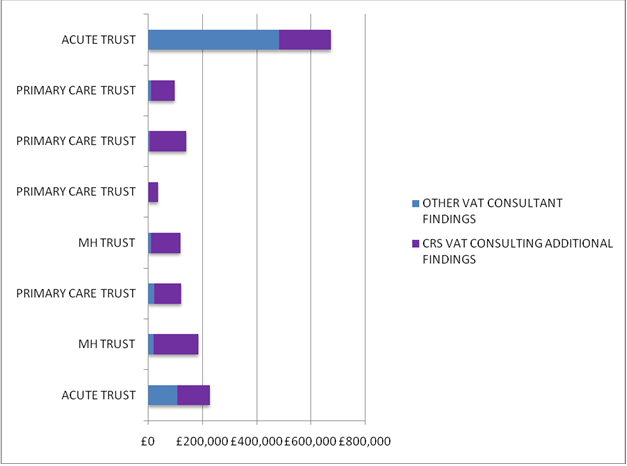

By reviewing the exact time periods and types of VAT as our main competitor, we produce substantial additional results.

The following table represents just eight of the latest contracted-out services (“COS”) VAT re-reviews which we have completed for the first nine months of 2009/10 (April to December) where the previous adviser had already carried out their VAT review.

On average, we have identified £140,000 more VAT recovery than the previous adviser.

Don’t forget that there is an annual deadline of the end of June 2010 to make sure that any COS VAT for the 2009/10 year is claimed, so please contact us as soon as possible in order to arrange a re-review.

NHS bodies should be aware of a newly published concession which may lead to a decrease in VAT being charged on nursing services which is currently eligible for recovery under the Contracted-Out Services (“COS”) rules.

HMRC have now permitted nursing agencies (or employment businesses providing nurses, midwives, and other health professionals) to exempt the supply of nursing staff and nursing auxiliaries supplied to an NHS body (provided that they are registered with an organisation approved by HMRC).

Qualifying suppliers providing nursing auxiliaries or care assistants may use the concession if the individuals they place undertake some direct form of medical care (such as administering drugs or taking blood pressures, for the final patient). However, the concession does not apply to supplies of general care assistants who are only involved in providing personal care such as catering, washing or dressing the patients.

In some cases, it may be in the interests of nursing agencies to continue to charge VAT, rather than to exempt their supplies.

For example, certain nursing agencies may be taxable businesses which are able to recover 100% of the VAT which they incur in respect of nursing and auxiliary staff which they supply (because they are supplied subject to VAT). Therefore, they may feel that their own VAT recovery will be restricted by adopting the concession to certain services. This is likely to lead to an increase in the costs to their NHS clients because of the irrecoverable VAT costs. As a result, there may be scope for certain NHS bodies to ask such agencies to continue to charge VAT on certain services described above. If the agencies agree, then NHS bodies may continue to recover the VAT on the costs of supplies of nursing and auxiliary services which they incur, (until at least the COS rules change).

If you would like further details regarding this concession, and the impact it may have on your NHS body’s recoverable VAT, please do not hesitate to contact us.

As stated in the article above, it is common knowledge that NHS bodies are able to recover VAT incurred on supplies of nursing staff (including qualified and non-qualified nurses/healthcare assistants) under COS heading 41 and admin/clerical grade staff (including receptionists, secretaries, etc) under COS heading 69.

However, in respect of temporary placements of health professionals described as ‘ODP’s’ and ‘ODA’s’, HMRC have recently sought clarification from their policy unit and have taken the view that the related VAT incurred by an NHS body is not recoverable.

We are currently seeking further clarification on this point, given that we understand these acronyms are in fact considered by many as nursing staff grades.

Following on from the submission of Fleming/Conde Nast VAT claims (the first anniversary of the 31 March 2009 deadline having now come and gone), the claims submitted on behalf of NHS bodies still appear to have a long way to go before they are settled.

At present, HMRC have stated that both the ‘Lennartz’ and ‘Wellington/BUPA’ elements of the Fleming claims are invalid. This is because in HMRC’s view, subsequent case law has meant that the decisions in these cases were either wrong or have been superseded.

HMRC invited CRS VAT Consulting along with other representative claimants to a meeting in London a few weeks ago to explain their decision on the Wellington/BUPA drugs issue with a view to finding some ‘common ground,’ however the obvious intention was to dissuade any claimant from taking the issue any further. It is however likely that at least one rejected claimant may submit a formal appeal to the VAT Tribunal.

Other elements of certain claims are still technically valid (e.g. prescription drugs, other drug sales, catering, etc), however HMRC have still not yet decided on the issue of whether the claimant Trusts or the SHAs have the right to pre-Trust claims. Until this issue is resolved, these elements of claims which are technically valid are also being held up.

In our last VAT report, we advised that the new procedures for compulsory online VAT return filing were not yet available to the NHS. HMRC have since stated that online filing will be applicable to the NHS, however the issue of how to file the accompanying VAT21 Form does not yet appear to have been resolved. We will therefore keep you informed as soon as further guidance is available.

Revenue and Customs Brief 09/10 announced their revised policy with regard to the supply of education by a university subsidiary trading company. HMRC have reviewed their policy on the treatment of supplies of education delivered by companies that are owned or controlled by a university, and have concluded that, in many cases where a university trading company provides education, they are acting as a ‘college, institution, school or hall of a university’ and in consequence are ‘eligible bodies’. This means that any education or training provided by the university subsidiary trading company is an exempt supply of education.

University trading companies which have been charging VAT on education and training services to NHS bodies in the past have benefitted from input tax recovery on associated costs. In turn, the VAT charged by these companies to NHS bodies has generally been eligible for recovery by the NHS recipient under the COS provisions.

This change in HMRC’s policy is therefore likely to lead to university trading companies having to increase their charges to NHS customers to take account of the VAT exempt status and therefore irrecoverable VAT on costs.

Following a recent ECJ decision, (Vereniging Noordelijke Land-en Tuinbouw Organisatie v Staatssecretaris van Financien (C-515/07) – (VNLTO)), and a meeting of the EU Council, it has been anounced by HMRC that from 22 January 2010, the use of the Lennartz mechanism will be restricted to circumstances where goods/services are to be put to both business and private use or use outside of the taxpayers normal activities. The previous UK application of Lennartz for non-business activities of taxpayers (including NHS bodies) will no longer be available and strictly speaking, has never been available.

By way of background, where a taxable person/taxpayer (including an NHS body) uses goods or services for both taxable business and non-business purposes (e.g. NHS healthcare), the normal course of action would be to apportion the VAT and recover only the amount which relates to taxable business use. The Lennartz mechanism (named after a 1992 ECJ decision) is an alternative procedure whereby the taxable person may, in some circumstances, choose to recover all of the VAT incurred, but consequently pay output tax on every VAT return to reflect the cost of the non-business use in the return period over the life of the asset.

As NHS bodies have mainly non-business activities (i.e. NHS healthcare), use of the Lennartz mechanism has been available in circumstances where there was a genuine and ongoing taxable business use of the goods in question in addition to non-business use.

From 22 January 2010, Lennartz accounting will only be available where:

- the goods are used in part for making taxable supplies, ; and

- they are also used in part for the private purposes of the trader or his staff, or, exceptionally, for other uses which are wholly outside the purposes of the taxpayer’s enterprise or undertaking

Taxpayers for whom Lennartz accounting has, strictly speaking, never been available would normally be expected to unravel the mechanism and adjust both any input tax claimed and any output tax accounted for accordingly. However, where a taxpayer has already applied Lennartz accounting on the basis of HMRC’s pre-VNLTO understanding of the law, the taxpayer may opt to continue using Lennartz accounting in respect of the assets concerned.

Those taxpayers who do not exercise this option must unravel the Lennartz accounting mechanism by adjusting both their output tax and corresponding input tax.

Taxpayers who are not permitted to use Lennartz accounting must apportion VAT incurred for both economic and non-economic activities on the basis of use and intended use from the date of this announcement. However, HMRC will consider claims from taxpayers who have already entered into binding commitments for projects on the understanding that Lennartz accounting will be available.

Following this decision, HMRC are now likely to reject Fleming/Conde-Nast VAT claims submitted using the Lennartz mechanism where these relate to business/non-business activities on the basis that the Lennartz mechanism has never been available in these circumstances.

NHS bodies should already be aware that when certain services are purchased from an overseas supplier, VAT must be accounted to HMRC (in Box 1 of the VAT Return) under the ‘Reverse Charge’ Procedure.

Recent changes have been made to the VAT Place of Supply rules of cross border services to business customers from 1 January 2010. The general rule used to be that the place of supply was the country in which the supplier belonged. Now, the place of supply is determined by the location of the customer.

There are still some exceptions to the general rule, but this procedure now applies to almost all services purchased from overseas.

The changes do not involve a new compliance procedure, but it is in the interests of NHS bodies to re-familiarise themselves as to how the Reverse Charge should be accounted for on the VAT return.

Depending upon the nature of the service, there may be scope to recover the equivalent amount in box 4 of the VAT return, if the VAT on the supply received is an eligible contracted–out service (COS). If the VAT is not COS VAT, a proportion of it may be recovered as input tax, dependent on the extent to which the supply relates to a taxable business activity (e.g. non-NHS equipment sales, catering, etc).

If you would like further detail regarding the Reverse Charges procedure or the impact of the Place of Supply rule changes, please do not hesitate to contact us.